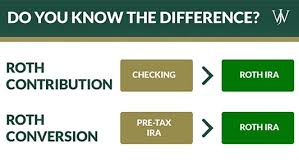

Rolling over a traditional IRA into a Roth IRA isn’t just a financial move—it’s a long-term strategy with powerful tax benefits. While these rollovers were all the rage a few years back, they’ve fallen off the radar for many. But for the right individual, they can still be a game-changer.

Here’s why: With a Roth IRA, your future withdrawals—including earnings—are entirely tax-free, provided you meet the rules. That’s especially appealing if you expect your tax rate to be higher in retirement. A rollover allows you to pay taxes on your contributions now, at today’s rates, rather than later when they might be higher.

Timing and circumstances matter, though. A rollover makes sense when you have funds to cover the tax hit without dipping into your IRA. It’s also crucial to consider your current tax bracket and retirement goals.

This strategy isn’t a one-size-fits-all solution. That’s where a trusted financial advisor steps in. Together, we’ll analyze your unique situation, crunch the numbers, and figure out if a Roth IRA conversion aligns with your goals.

The market might have forgotten about this strategy, but the benefits are still very much alive for those who qualify. Let’s explore whether this opportunity is right for you. Reach out today!

We would love to work with you to accomplish your goals. Please contact us through the contact page HERE, directly to Joe Lind at jlind@dinergywealth.com or call Joe at 513-878-0195. Let’s grow together!